Driving the Rollercoaster: A 12 months within the Lifetime of 30-12 months Mortgage Charges (2024 – Hypothetical)

Associated Articles: Driving the Rollercoaster: A 12 months within the Lifetime of 30-12 months Mortgage Charges (2024 – Hypothetical)

Introduction

On this auspicious event, we’re delighted to delve into the intriguing subject associated to Driving the Rollercoaster: A 12 months within the Lifetime of 30-12 months Mortgage Charges (2024 – Hypothetical). Let’s weave attention-grabbing data and supply contemporary views to the readers.

Desk of Content material

Driving the Rollercoaster: A 12 months within the Lifetime of 30-12 months Mortgage Charges (2024 – Hypothetical)

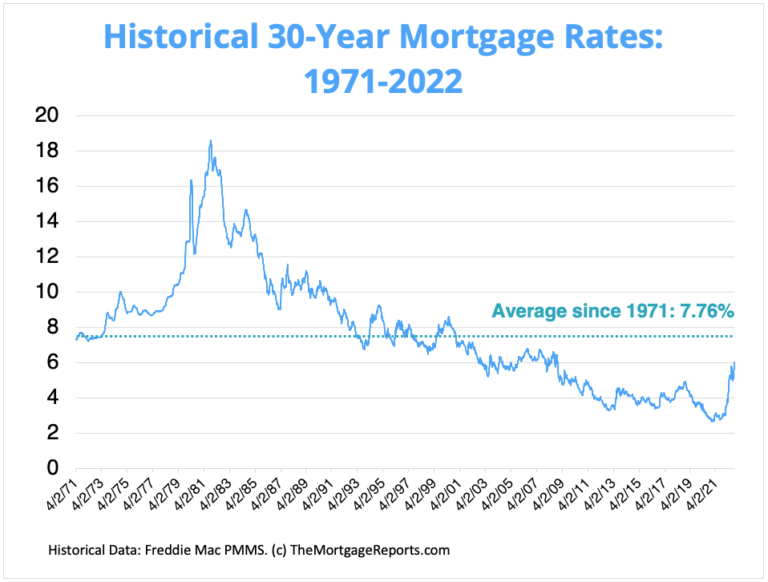

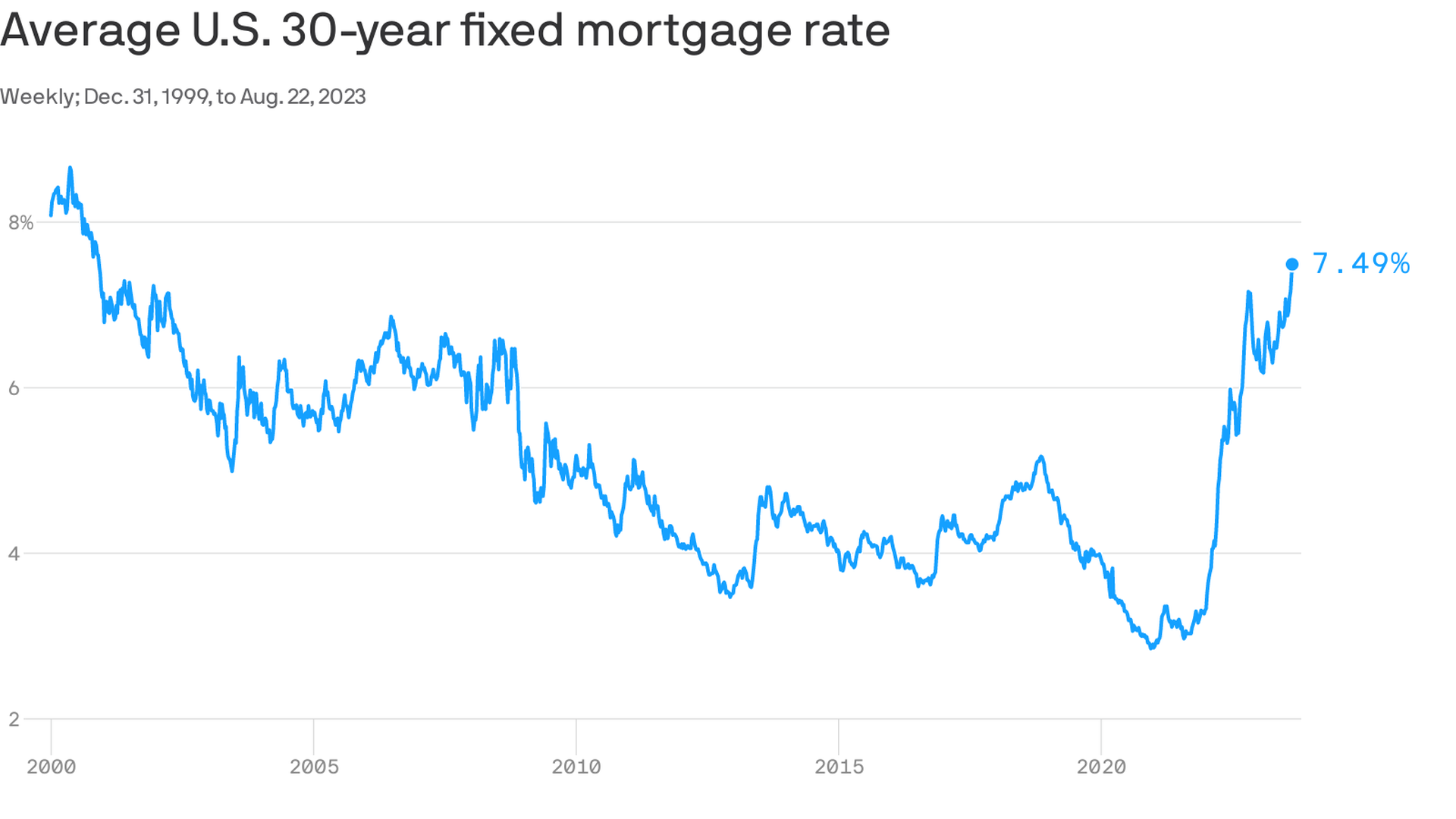

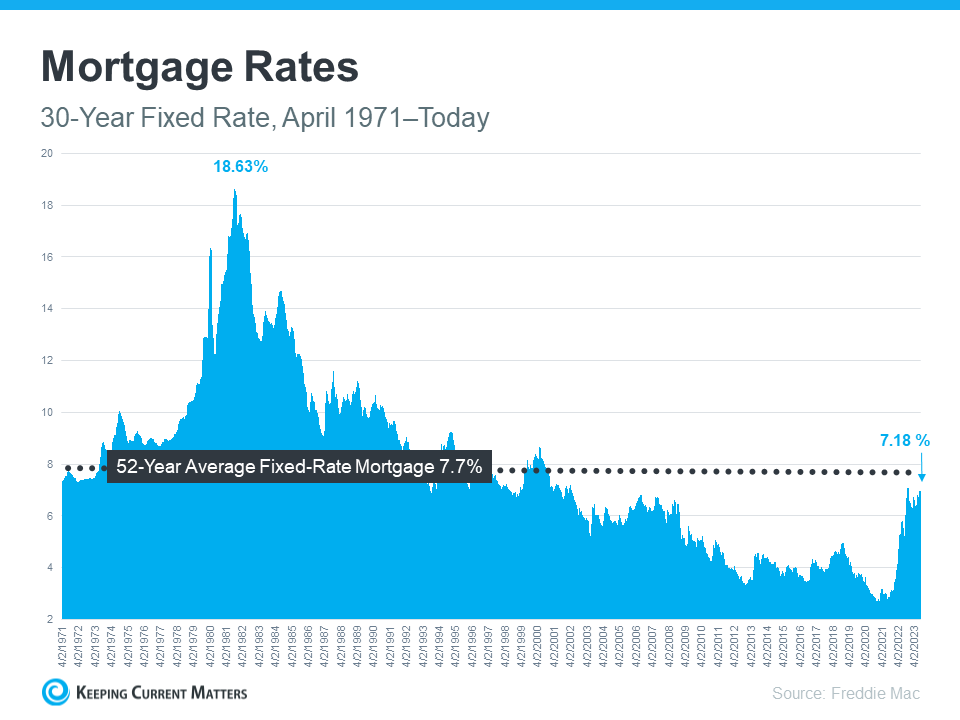

The 30-year fixed-rate mortgage is the bedrock of the American dream of homeownership. Its stability, predictability, and comparatively lengthy amortization interval make it a well-liked alternative for hundreds of thousands. Nonetheless, the rate of interest connected to this mortgage is something however steady. Fluctuations out there, pushed by financial indicators, authorities insurance policies, and international occasions, can considerably affect the price of borrowing and the affordability of housing. This text analyzes a hypothetical one-year interval (let’s assume January 2024 to December 2024) for example the dynamic nature of 30-year mortgage charges and the components that affect them. Please word: All charges and information offered on this article are hypothetical and for illustrative functions solely. Precise charges will range based mostly on quite a few components.

January 2024: The Calm Earlier than the Storm (Hypothetical Charge: 6.5%)

We start our journey in January 2024, with a hypothetical 30-year mounted mortgage price of 6.5%. This price, whereas larger than historic lows, displays a comparatively steady market. The earlier 12 months noticed a interval of rising charges, fueled by persistent inflation and the Federal Reserve’s efforts to fight it by rate of interest hikes. The market is cautiously optimistic, with some analysts predicting a possible leveling off of charges, whereas others foresee additional will increase. Demand for housing stays comparatively sturdy, although barely softened by the upper borrowing prices. The general financial outlook is unsure, with considerations about potential recession looming.

February – April 2024: A Gradual Ascent (Hypothetical Charge Vary: 6.75% – 7.25%)

February brings a slight uptick in charges, reaching 6.75%. That is attributed to stronger-than-expected inflation information, prompting the Federal Reserve to sign a continuation of its aggressive financial coverage. March sees an extra improve to 7%, fueled by geopolitical instability and ongoing provide chain disruptions. By April, charges climb to 7.25%, reflecting the rising considerations about inflation and the potential for additional rate of interest hikes from the Federal Reserve. The housing market begins to point out indicators of cooling, with fewer gross sales and a slight lower in dwelling costs in some areas.

Could – July 2024: A Interval of Volatility (Hypothetical Charge Vary: 7.00% – 7.75%)

Could brings a stunning dip in charges to 7%, as unexpectedly constructive financial information suggests inflation could also be peaking. This non permanent reduction is short-lived, nonetheless, as June sees a pointy improve to 7.5% on account of a renewed surge in inflation. July brings additional volatility, with charges fluctuating between 7.25% and seven.75%, reflecting the uncertainty out there. The housing market continues to decelerate, with patrons changing into more and more price-sensitive. The affect of upper charges on affordability is changing into more and more evident.

August – October 2024: A Plateau and Indicators of Stabilization (Hypothetical Charge Vary: 7.5% – 7.75%)

August and September see charges plateau round 7.5% – 7.75%. The Federal Reserve maintains its hawkish stance, however the market begins to anticipate a possible slowdown in price hikes. October brings a slight lower to 7.5%, reflecting a rising perception that inflation is lastly below management. This era of relative stability presents a glimmer of hope for potential homebuyers, though charges stay considerably larger than these seen in earlier years.

November – December 2024: A Cautious Optimism (Hypothetical Charge Vary: 7.25% – 7.00%)

November brings an extra lower to 7.25%, fueled by constructive financial information and expectations that the Federal Reserve may pause its price hikes. December concludes the 12 months with a price of seven.00%, representing a modest decline from the height in July. Whereas charges stay elevated, the downward development suggests a possible easing of financial coverage within the coming 12 months. The housing market exhibits indicators of restoration, with elevated exercise in some segments.

Components Influencing 30-12 months Mortgage Charges:

A number of key components affect the fluctuations noticed in our hypothetical one-year chart:

- Inflation: The first driver of rate of interest modifications. Excessive inflation prompts central banks to boost rates of interest to chill down the financial system.

- Federal Reserve Coverage: The Federal Reserve’s actions, significantly its goal federal funds price, immediately affect mortgage charges.

- Financial Development: Sturdy financial progress can result in larger inflation and consequently larger rates of interest. Conversely, weak financial progress can result in decrease charges.

- Unemployment Charge: Low unemployment can contribute to inflationary strain, resulting in larger charges.

- International Financial Situations: Worldwide occasions, resembling geopolitical instability or international recessions, can considerably affect mortgage charges.

- Authorities Insurance policies: Authorities rules and interventions within the housing market can affect demand and provide, not directly affecting charges.

- Investor Sentiment: Market confidence and investor expectations play an important position in shaping rate of interest actions.

Impression on Homebuyers:

The fluctuations in mortgage charges all year long considerably affect homebuyers. Greater charges improve the month-to-month mortgage funds, lowering affordability and probably limiting the pool of certified patrons. This may result in decreased demand, probably impacting dwelling costs. Conversely, decrease charges can stimulate demand and drive up costs. The volatility skilled all year long creates uncertainty for each patrons and sellers, making it essential to fastidiously contemplate the timing of buying a house.

Conclusion:

The hypothetical one-year chart of 30-year mortgage charges illustrates the complicated and dynamic nature of the mortgage market. Quite a few interconnected components affect price fluctuations, making a difficult surroundings for homebuyers and the broader financial system. Understanding these components and their affect is essential for making knowledgeable selections about homeownership. Whereas this text presents a hypothetical state of affairs, it highlights the significance of staying knowledgeable about financial traits and market circumstances to navigate the complexities of the mortgage market efficiently. It’s at all times advisable to seek the advice of with a monetary advisor and mortgage skilled earlier than making any main monetary selections. Keep in mind, this text is for informational functions solely and shouldn’t be thought-about monetary recommendation.

Closure

Thus, we hope this text has offered priceless insights into Driving the Rollercoaster: A 12 months within the Lifetime of 30-12 months Mortgage Charges (2024 – Hypothetical). We admire your consideration to our article. See you in our subsequent article!