The Usually Accepted Chart of Accounts: A Basis for Monetary Reporting

Associated Articles: The Usually Accepted Chart of Accounts: A Basis for Monetary Reporting

Introduction

With enthusiasm, let’s navigate via the intriguing matter associated to The Usually Accepted Chart of Accounts: A Basis for Monetary Reporting. Let’s weave fascinating info and provide recent views to the readers.

Desk of Content material

The Usually Accepted Chart of Accounts: A Basis for Monetary Reporting

A chart of accounts (COA) is the spine of any group’s monetary reporting system. It is a structured listing of all of the accounts utilized by a enterprise to report its monetary transactions. Whereas the precise accounts and their numbering system can range relying on the {industry}, measurement, and complexity of the group, the underlying ideas stay constant, significantly when adhering to usually accepted accounting ideas (GAAP) or Worldwide Monetary Reporting Requirements (IFRS). This text explores the important thing parts of a usually accepted chart of accounts, its construction, widespread account classifications, and the significance of its constant software.

The Goal and Significance of a Chart of Accounts

A well-designed COA serves a number of essential functions:

- Group of Monetary Knowledge: It gives a scientific solution to categorize and observe all monetary transactions, making certain that monetary info is quickly accessible and simply comprehensible. This facilitates correct monetary reporting and evaluation.

- Monetary Assertion Preparation: The COA is important for producing correct and dependable monetary statements, together with the stability sheet, earnings assertion, and assertion of money flows. Every transaction is recorded within the applicable account, permitting for the aggregation of knowledge wanted for these statements.

- Inside Management: A correctly designed COA contributes to a robust inner management system by offering a framework for monitoring monetary exercise and stopping errors or fraud. Clear account segregation helps to restrict entry and enhance oversight.

- Determination-Making: The knowledge contained throughout the COA gives crucial knowledge for administration decision-making. By analyzing the information, companies can determine developments, assess profitability, and make knowledgeable choices relating to useful resource allocation and strategic planning.

- Auditing and Compliance: A constant and well-documented COA simplifies the audit course of and ensures compliance with related accounting requirements and laws. Auditors can simply confirm the accuracy and completeness of economic information.

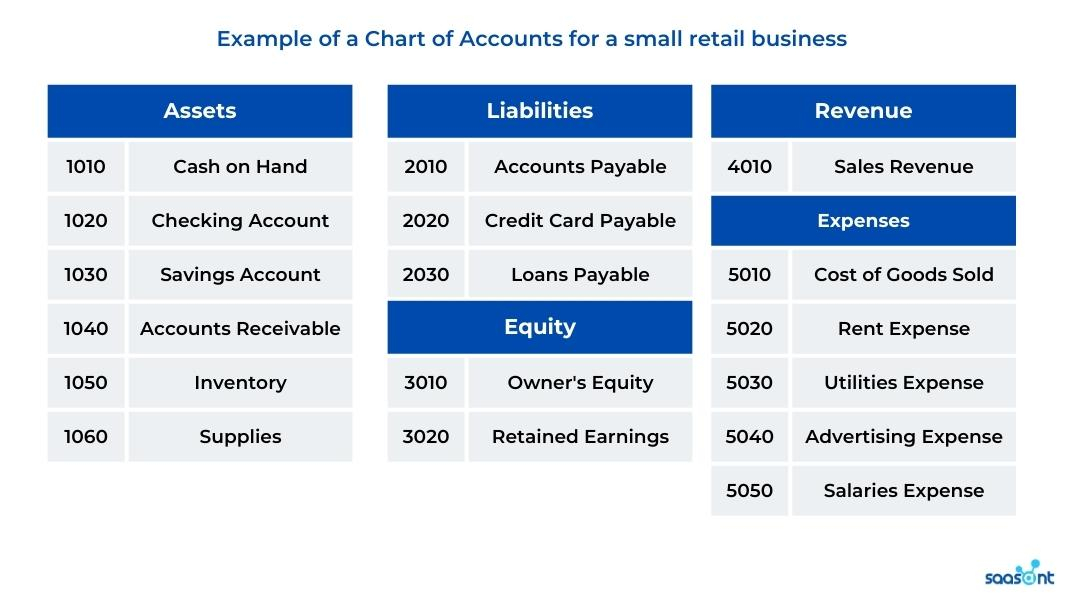

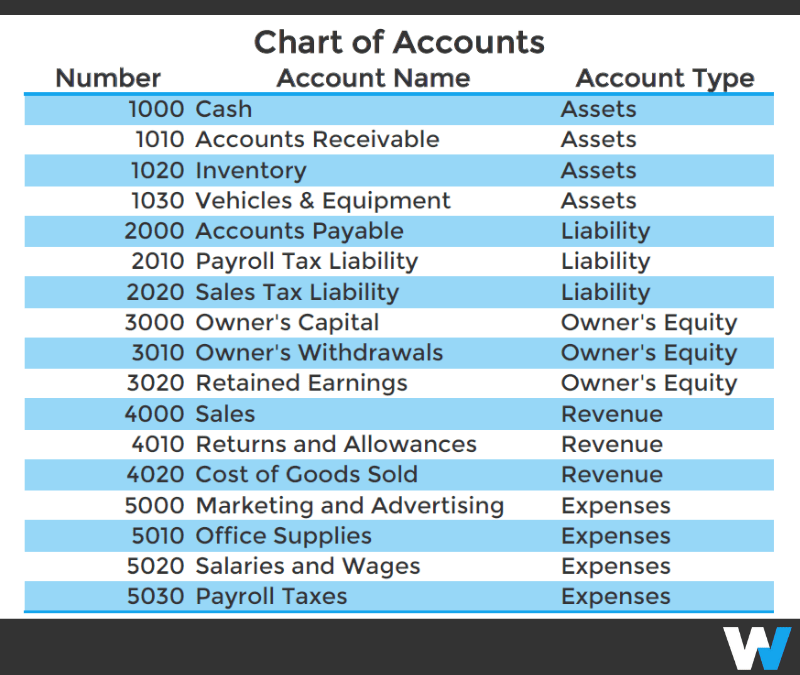

Construction and Classification of a Usually Accepted Chart of Accounts

A usually accepted chart of accounts usually follows a hierarchical construction, categorizing accounts into main teams and subgroups. This construction facilitates simple navigation and reporting. The precise construction could range, however widespread classifications embody:

-

Belongings: These signify what an organization owns. Belongings are additional categorized into:

- Present Belongings: Belongings anticipated to be transformed into money or used up inside one 12 months (e.g., money, accounts receivable, stock, pay as you go bills).

- Non-Present Belongings (Lengthy-term Belongings): Belongings anticipated for use for multiple 12 months (e.g., property, plant, and tools (PP&E), intangible property, long-term investments).

-

Liabilities: These signify what an organization owes to others. Much like property, liabilities are divided into:

- Present Liabilities: Obligations due inside one 12 months (e.g., accounts payable, salaries payable, short-term loans).

- Non-Present Liabilities (Lengthy-term Liabilities): Obligations due in multiple 12 months (e.g., long-term loans, bonds payable).

-

Fairness: This represents the homeowners’ stake within the firm. For firms, this contains:

- Widespread Inventory: Represents the possession shares issued to shareholders.

- Retained Earnings: Amassed income that haven’t been distributed as dividends.

-

Income: This represents the earnings generated from the corporate’s major operations (e.g., gross sales income, service income).

-

Bills: These signify the prices incurred in producing income (e.g., value of products offered, salaries expense, hire expense, utilities expense, advertising expense).

Particular Account Examples inside Every Class:

Whereas the precise naming conventions can differ, the next examples illustrate widespread accounts inside every main class:

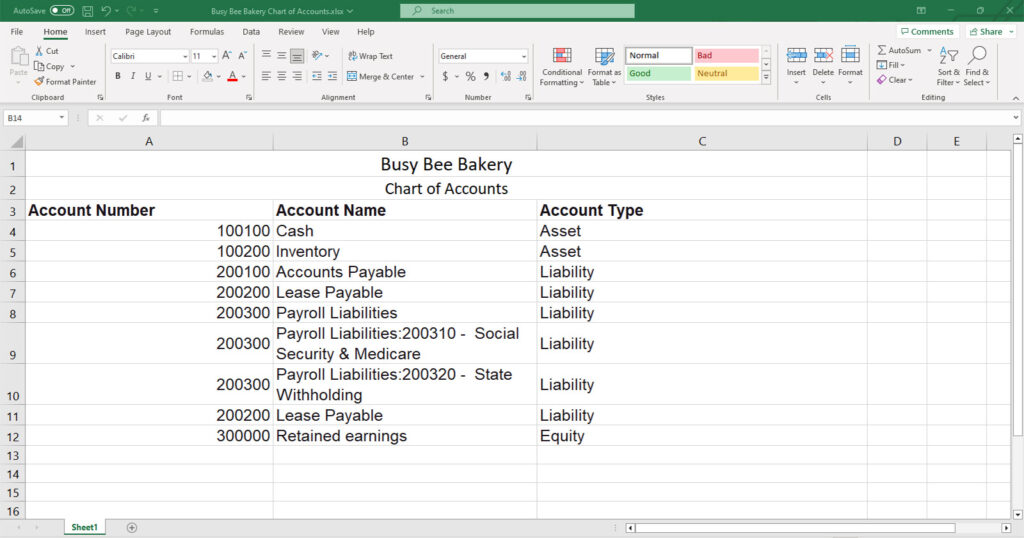

Belongings:

- 1000 Money: Consists of checking, financial savings, and petty money accounts.

- 1100 Accounts Receivable: Cash owed to the corporate by prospects.

- 1200 Stock: Items held on the market.

- 1300 Pay as you go Bills: Bills paid upfront (e.g., insurance coverage, hire).

- 1400 Property, Plant, and Gear (PP&E): Land, buildings, equipment, and tools.

- 1500 Amassed Depreciation: Contra-asset account lowering the worth of PP&E.

- 1600 Intangible Belongings: Patents, copyrights, emblems.

Liabilities:

- 2000 Accounts Payable: Cash owed to suppliers.

- 2100 Salaries Payable: Wages owed to staff.

- 2200 Notes Payable: Brief-term and long-term loans.

- 2300 Bonds Payable: Lengthy-term debt issued to traders.

Fairness:

- 3000 Widespread Inventory: Shares issued to shareholders.

- 3100 Retained Earnings: Amassed income.

Income:

- 4000 Gross sales Income: Income from the sale of products.

- 4100 Service Income: Income from companies offered.

Bills:

- 5000 Value of Items Offered (COGS): Direct prices related to producing items.

- 5100 Salaries Expense: Wages paid to staff.

- 5200 Hire Expense: Value of renting premises.

- 5300 Utilities Expense: Value of electrical energy, water, and fuel.

- 5400 Advertising and marketing Expense: Prices related to promoting and promotion.

- 5500 Depreciation Expense: Allocation of the price of PP&E over its helpful life.

Selecting the Proper Chart of Accounts

The choice of an appropriate COA relies on varied elements, together with:

- Trade: Totally different industries have distinctive accounting wants, requiring particular accounts to trace industry-specific transactions.

- Firm Measurement: Bigger corporations usually require extra detailed and sophisticated COAs than smaller companies.

- Accounting Software program: The chosen accounting software program could dictate the construction and naming conventions of the COA.

- Administration Reporting Necessities: The COA must be designed to assist the precise reporting wants of administration.

Sustaining and Updating the Chart of Accounts

A COA is just not a static doc. It wants common evaluate and updates to replicate adjustments within the enterprise’s operations, accounting requirements, and reporting necessities. Including new accounts, modifying current ones, or retiring out of date accounts are all crucial steps to take care of the accuracy and relevance of the COA. Correct documentation of those adjustments is essential for sustaining auditability and consistency.

Conclusion

The widely accepted chart of accounts is a elementary device for efficient monetary administration. A well-designed and maintained COA is essential for correct monetary reporting, inner management, decision-making, and compliance with accounting requirements. By understanding the construction, classifications, and ideas of a usually accepted COA, companies can set up a strong basis for his or her monetary reporting system, making certain the reliability and integrity of their monetary info. Common evaluate and updates are important to maintain the COA aligned with the evolving wants of the group.

:max_bytes(150000):strip_icc()/chart-of-accounts-984cd9454c364932b0cba045f56a6bb1.jpg)

:max_bytes(150000):strip_icc()/chart-accounts-4117638b1b6246d7847ca4f2030d4ee8.jpg)

Closure

Thus, we hope this text has offered priceless insights into The Usually Accepted Chart of Accounts: A Basis for Monetary Reporting. We admire your consideration to our article. See you in our subsequent article!